Over-65 Health Insurance: Medicare and Medicaid Explained

- Compass Health Consultants®

- May 21

- 7 min read

Once you turn 65 or qualify due to disability, Medicare becomes your primary health insurance option, providing comprehensive coverage through federal programs. Understanding Medicare's parts, enrollment periods, and costs—plus how Medicaid can supplement coverage for lower-income seniors—ensures you maximize benefits while minimizing out-of-pocket expenses during retirement years.

Understanding Medicare Parts A, B, C, and D

Medicare consists of four distinct parts, each covering different aspects of healthcare:

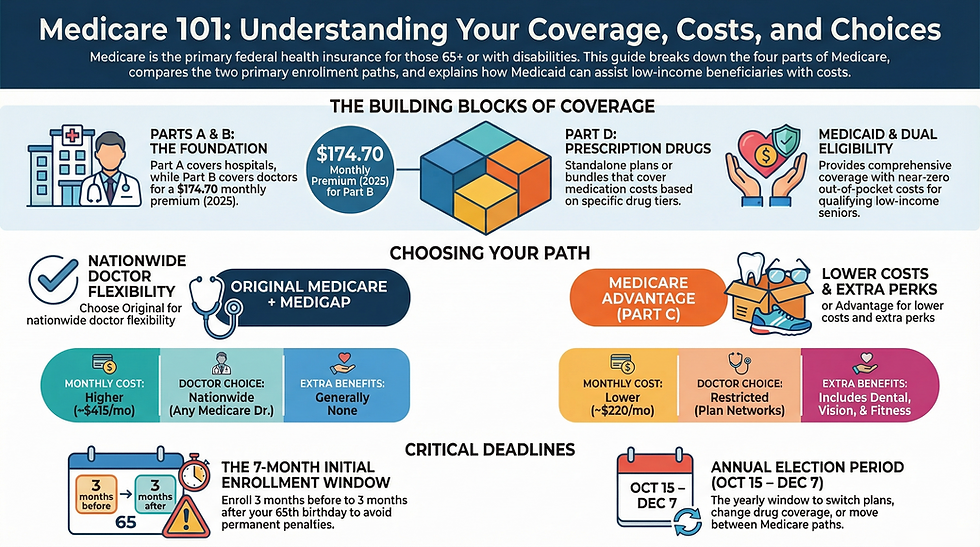

Part A - Hospital Insurance: Covers inpatient hospital stays, skilled nursing facility care (following hospital stays), hospice care, and some home health services. Most people pay no premium for Part A if they or their spouse paid Medicare taxes for 10+ years while working. The 2025 deductible is $1,632 per benefit period, with no coinsurance for the first 60 days of hospitalization.

Part B - Medical Insurance: Covers doctor visits, outpatient care, preventive services, durable medical equipment, and some home health services. Standard monthly premium is $174.70 in 2025, though high earners pay more through Income-Related Monthly Adjustment Amounts (IRMAA)—up to $594/month for individuals earning over $500,000. After meeting the $240 annual deductible, you typically pay 20% coinsurance for most services.

Part C - Medicare Advantage: Private insurance alternative that bundles Parts A, B, and usually D into one plan. These plans often include additional benefits like dental, vision, and hearing coverage that Original Medicare doesn't provide. However, Medicare Advantage uses networks (HMO, PPO, or PFFS), potentially limiting your choice of doctors and hospitals. Premiums range from $0-$200/month depending on the plan and your location, plus any Part B premium.

Part D - Prescription Drug Coverage: Standalone prescription drug coverage available through private insurers, or included in most Medicare Advantage plans. Monthly premiums average $40-$80 but vary significantly by plan and location. Coverage is organized into drug tiers (generic, preferred brand, non-preferred brand, specialty) with different copays or coinsurance for each tier. Most plans have a coverage gap (donut hole) where you pay higher costs after reaching initial coverage limits until catastrophic coverage begins.

Original Medicare vs. Medicare Advantage: Choosing Your Path

You have two main options for receiving Medicare benefits:

Original Medicare (Parts A + B): Federal government directly provides coverage. You can see any doctor or hospital nationwide that accepts Medicare—no networks, no referrals needed. However, Original Medicare has no out-of-pocket maximum and doesn't cover prescriptions, dental, vision, or hearing. Most people add a Part D plan for prescriptions and often purchase Medigap (Medicare Supplement) insurance to cover the 20% coinsurance and other gaps.

Medicare Advantage (Part C): Private insurers provide all Medicare benefits through a single plan. These plans include an annual out-of-pocket maximum (typically $8,000-$8,850) for better financial protection. Most include prescription coverage and extra benefits like dental, vision, fitness programs, and over-the-counter allowances. The trade-off: you must use network providers (except emergencies) and may need referrals for specialists. Plan networks and benefits change annually during the October 15 - December 7 enrollment period.

Medicare Enrollment Periods: Critical Timing

Missing Medicare enrollment deadlines can result in lifetime penalties and coverage gaps:

Initial Enrollment Period (IEP): 7-month window beginning 3 months before your 65th birthday month, including your birthday month, and ending 3 months after. Most people should enroll during the 3 months before turning 65 to ensure coverage starts on their birthday. Missing this window triggers late enrollment penalties.

Late Enrollment Penalties: If you don't enroll in Part B during your IEP and don't have creditable coverage (employer plan), you'll pay a 10% penalty for each 12-month period you delayed, added to your Part B premium forever. Part D penalties are 1% of the national base premium for each month delayed, also permanent.

Annual Election Period (AEP): October 15 - December 7 each year. During this time, you can switch between Original Medicare and Medicare Advantage, change Medicare Advantage plans, join or switch Part D plans, or add/drop Medigap policies (in some states). Changes take effect January 1.

Special Enrollment Periods: Available when you move out of your plan's service area, lose employer coverage, qualify for Medicaid or Extra Help, or live in a nursing home. These allow enrollment changes outside the annual period.

Medicaid: Supplemental Coverage for Low-Income Seniors

Medicaid is a joint federal-state program providing health coverage for low-income individuals, including seniors. Dual eligible beneficiaries—people who qualify for both Medicare and Medicaid—receive comprehensive coverage with minimal out-of-pocket costs:

What Medicaid Covers for Dual Eligibles:

• Pays Medicare Part B premiums (saving $174.70/month in 2025)

• Covers Medicare deductibles and coinsurance, reducing out-of-pocket costs to near zero

• Provides prescription drug coverage through state programs

• Includes services Medicare doesn't cover: dental care, vision care, hearing aids, long-term care

• Covers nursing home and in-home care costs for qualifying individuals

Medicaid Eligibility: Income and asset limits vary by state. Generally, individuals earning below 138% of the Federal Poverty Level ($20,780 in 2025) may qualify, though some states use different thresholds. Asset limits typically exclude your primary home, one vehicle, and modest savings. Application is through your state Medicaid office, and coverage can be retroactive up to 3 months.

Important: Dual eligible status provides the most comprehensive health coverage available, combining Medicare's broad provider access with Medicaid's financial assistance. If you think you might qualify, apply immediately—the savings can be substantial.

Real-World Cost Comparison

Example 1: Robert, Age 67, Original Medicare + Medigap

Monthly costs:

• Part B premium: $174.70

• Medigap Plan G: $185

• Part D drug plan: $55

Total: $414.70/month ($4,976 annually) with minimal out-of-pocket costs when using healthcare

Example 2: Maria, Age 68, Medicare Advantage

Monthly costs:

• Part B premium: $174.70

• Medicare Advantage plan (includes Part D): $45

Total: $219.70/month ($2,636 annually)

Plus when using care: $15-40 copays per visit, up to $7,550 annual out-of-pocket maximum. However, plan includes dental ($1,500 allowance), vision ($200 allowance), and gym membership.

Medicare Coverage: Benefits and Considerations

Medicare Advantages

Important Considerations

Guaranteed coverage at 65 regardless of health status or pre-existing conditions

Late enrollment penalties are permanent—missing deadlines costs you for life

Original Medicare accepted nationwide at nearly all providers and hospitals

Part B covers only 80% of costs—20% coinsurance can add up without Medigap

Medicare Advantage plans include out-of-pocket maximums for financial protection

Medicare Advantage networks limit provider choice and may require referrals

Preventive services covered at 100% with no cost-sharing on both paths

Original Medicare has no out-of-pocket maximum, exposing you to unlimited costs

Part D prescription coverage keeps medication costs manageable for most people

Coverage gap (donut hole) increases prescription costs mid-year until catastrophic kicks in

Can switch between Original Medicare and Medicare Advantage annually

Medigap policies guaranteed issue only during initial enrollment—harder to get later

Dual eligibles combining Medicare and Medicaid get comprehensive coverage at minimal cost

Medicare doesn't cover long-term care, dental, vision, or hearing (Original Medicare)

Frequently Asked Questions About Medicare

When should I enroll in Medicare if I'm still working at 65?

If you have creditable employer coverage through your or your spouse's current employment at a company with 20+ employees, you can delay Medicare enrollment without penalties. However, you should enroll in Part A (if premium-free) since it doesn't conflict with HSAs or most employer plans. Enroll in Part B within 8 months of leaving the job or losing coverage to avoid late penalties. Smaller employers: their coverage may not be creditable—verify with HR and enroll in Medicare at 65.

Should I choose Original Medicare or Medicare Advantage?

Choose Original Medicare if you want maximum flexibility, travel frequently, see specialists regularly, or have complex health needs requiring access to any provider nationwide. Add Medigap for comprehensive coverage. Choose Medicare Advantage if you prefer lower monthly costs, want extra benefits like dental and vision, stay in one area, and don't mind network restrictions. Your choice isn't permanent—you can switch during the annual election period October 15 - December 7.

What is Medigap and do I need it?

Medigap (Medicare Supplement Insurance) is private insurance that covers gaps in Original Medicare—primarily the 20% coinsurance on Part B services. Plans are standardized (Plan G is most popular) with premiums ranging from $100-$300/month depending on age and location. You should consider Medigap if you choose Original Medicare and want predictable costs without surprise bills. Enroll during your 6-month Medigap Open Enrollment Period starting when you turn 65 and enroll in Part B—this guarantees acceptance regardless of health. After this window, insurers can deny coverage or charge more based on health conditions.

Can I have both employer insurance and Medicare?

Yes. If you're still working at 65 with employer coverage, coordination of benefits rules determine which insurance pays first. For employers with 20+ employees, employer coverage is primary and Medicare is secondary. For smaller employers, Medicare is primary. Many people enroll in Part A (if premium-free) while keeping employer coverage, then add Part B when they retire. Consult your HR department before making enrollment decisions to understand how coverage coordinates.

What happens if I can't afford Medicare premiums?

Several programs help low-income Medicare beneficiaries. Medicaid pays Part B premiums and cost-sharing for dual eligibles. Medicare Savings Programs (QMB, SLMB, QI) pay some or all Medicare premiums for people earning up to 135% of poverty level. Extra Help (Low-Income Subsidy) reduces Part D prescription costs significantly. State Pharmaceutical Assistance Programs provide additional help. Contact your State Health Insurance Assistance Program (SHIP) for free guidance on available assistance programs. Don't go without coverage—help is available.

How do I know which Part D prescription plan to choose?

Use Medicare's Plan Finder tool at Medicare.gov to compare Part D plans in your area. Enter all your current medications, and the tool calculates your total annual costs (premiums plus copays) for each plan. Choose the plan with the lowest total cost that includes your drugs on its formulary and has convenient pharmacies in your network. Review your plan annually during the October 15 - December 7 enrollment period, as formularies and costs change. Don't just compare premiums—total drug costs matter more.

Key Takeaways

• Medicare eligibility begins at 65 or earlier with qualifying disabilities

• Part A covers hospitals, Part B covers doctors, Part D covers prescriptions

• Choose Original Medicare for flexibility or Medicare Advantage for lower costs and extra benefits

• Enroll during 7-month Initial Enrollment Period to avoid permanent late penalties

• Medicaid supplements Medicare for low-income seniors (dual eligible status)

• Switch plans annually during October 15 - December 7 Annual Election Period

Comments